The premise for investing is pretty simple: to grow your money. It’s as simple as the reason for eating: to satisfy your hunger. Yet, choosing from the myriad investments out there can be as confusing as choosing among the thousands of items stocked on grocery store shelves.

The fact is not everything is good for you. How can you tell? One qualifier to consider: the source.

The origin of our investments matter. Perhaps, as much as it matters for our food.

For a minute, consider the apple I’m eating as I write this. It was organically grown at a local apple orchard. No pesticides. No underpaid labor. That information about its origin is valuable. For one, organic produce is shown to be more nutritious. Plus, buying organic is important as apples are a common staple on the “dirty dozen” list of produce that is often saturated with toxic pesticides. Not to mention giving my money directly to a farmer means more to me than giving it to a corporation practicing industrial farming.

We all know some foods are designed to turn a profit more than enrich the health of the consumer. Unfortunately, it can take a while for the science to reach the masses. Heck, everything from cigarettes to Coca-Cola have been marketed as healthy.

To live a healthy life is what we ask of our food. What do we ask of our investments?

There are parallels between the food and finance industries, and our relationship to both as consumers. After all, what goes in your mouth will influence your health just as what goes in your portfolio will influence your wealth.

I thought of that similarity after reading Trillions: How a Band of Wall Street Renegades Invented the Index Fund and Chanced Finance Forever by journalist Robin Wigglesworth.

The book covers the academic research that forms the basis of index funds — chalk full of Nobel Laureates like Harry Markowitz, William Sharpe and Eugene Fama — and all the key industry innovators and players — Wells Fargo, John Bogle and Vanguard, Lawrence Fink and BlackRock, etc. — that have contributed to passively managed funds overtaking the investment industry.

Full disclosure: I was given a review copy of Trillions by the publisher. I’m under no obligation to promote it or provide any type of review. I suppose this is a review of sorts, but it’s more of an exploration of the story the book tells as it relates to the investments we choose to buy. (For the record though, I really enjoyed it!)

The Uncomfortable Truth

Index funds were born out of objective academic research on how markets work and designed so that average investors can take full advantage of that information. The same can’t be said for a lot of other funds.

As Wigglesworth puts it:

“The finance industry has historically been adept at inventing new products that line its own pockets more than those on Main Street. The index fund is a rare exception to the rule.”

A very brief history of index funds goes like this:

The French mathematician Louis Jean-Baptiste Alphonse Bachelier wrote a doctoral thesis in 1900 (!) proving that financial securities move randomly. The baton of Bachelier’s discovery was passed along over the next six decades between the likes of Markowitz, Sharpe, Fama and others, leading to the notion that it’s all but impossible to reliably pick winning stocks.

Expressed creatively by Burton Malkiel in his classic book, A Random Walk Down Wall Street:

“A blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts.”

Professionals who are paid to select the best performers in the market more often don’t, which is what Wigglesworth calls the “uncomfortable truth.” Therefore, investors would be better off over time buying the market. With that knowledge in hand, people like Vanguard founder Jack Bogle worked hard to launch cheap funds that offered market averages to the public.

In summary, Wigglesworth writes:

“The genesis of index funds was the realization that most people–whether experienced professional money managers, a dentist investing for their retirement, or unemployed twentysomethings day-trading to make a quick buck — make terrible investors. The best long-term results come from buying a big, well-diversified portfolio of financial securities, and trading as little as possible. Jack Bogle built a vast financial empire around these two basic principles.”

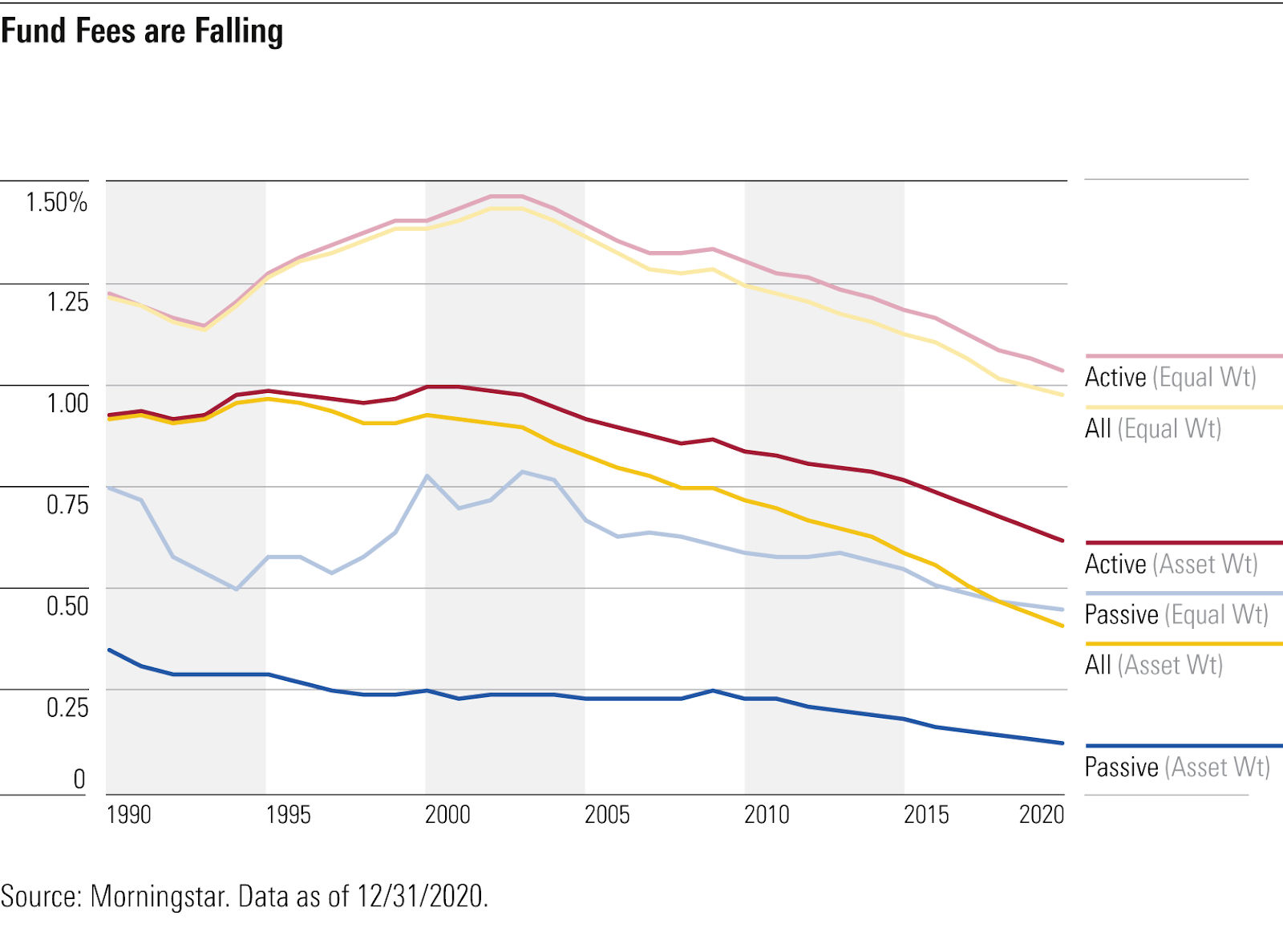

Cost also makes a difference. The more you pay in fees, the less of the fund’s return you get to keep. By simply tracking the market, an index fund can charge very little as it doesn’t have to pay anyone to select securities and constantly make trades.

Compare that to other funds that are built on the idea of skilled fund managers being able to find market opportunities and charge a higher price for their “expertise.”

What Wigglesworth deftly conveys is the amount of pushback these academically proven principles received by the old guards of Wall Street.

I hate to put it so sophomorically, I really do, but here it goes: The finance industry likes to smell its own farts. (Sorry!) Some people just like to clothe themselves in the illusion of superior skill. So much so, that any counter evidence is perceived as a threat.

Consider the anecdote Wigglesworth shares about the Wells Fargo analyst Willam Fouse, who tried repeatedly to get different firms to create passive funds. One boss tells him incredulously: “Goddammit Fouse, you’re trying to turn my business into a science.”

As an investor, isn’t that what we want? Hard evidence over irrational confidence?

We can see their fears realized, as the rise of passively managed funds has steadily eaten away fund fees.

Less money for Wall St. yachts

It’s worthwhile then to know the intentions of those selling you an investment.

Wigglesworth recounts a common industry reaction to index funds:

“[A]s the writer Upton Sinclair once observed, it is difficult to get someone to understand something when their salary depends on them not understanding it. ‘If people start believing this random-walk garbage and switch to index funds, a lot of $80,000-a-year portfolio managers and analysts will be replaced by $16,000-a-year computer clerks. It just can’t happen,’ one anonymous mutual fund manager griped to the Wall Street Journal in 1973.”

Turning a Dollar Into a Million

In his famous essay, “The Pleasures of Eating,” the poet and environmental activist Wendell Berry said, “eating is an agricultural act”, meaning that what you choose to eat has real influence on food production. To be ignorant of that fact, he says, makes you vulnerable to the influence of the food industry, which often places profit and volume over quality and health.

Investing is a capitalistic act. Your individual investment decisions have an impact on the investment industry as well as on the quality of your portfolio. Where you put your savings can influence the well-being of the industry — promote funds that are designed to help investors, keep financial advisers who actually care about you in business — and ultimately your own well-being.

In all fairness, there are legitimate concerns about the growing influence of index funds, which is discussed by Wigglesworth in Trillions. For example, they could be warping the markets they are meant to emulate and accumulating far too much corporate voting power. However, all of that is far beyond the scope of this blog.

Ultimately, investing requires a little learning and soul searching.

Not everything available to you — be it by a professional, or in your 401(k), or in an account you manage yourself — is necessarily aligned with your best interest. You should know why you own what you own.

Of course, ego isn’t an easy thing to extract even as a professional. Understanding how markets work can help add a dash of humility into our thinking. Too often we succumb to our own biases that make us think we know more than we actually do.

One of the many interesting anecdotes in Trillions is a reference to a speech by Warren Buffett, during which he asked listeners to imagine a nationwide coin-flipping contest. Each American puts in $1 each day. Those who guess wrong are eliminated while the winners continue playing. Statistically, after 20 days, 215 players should remain, having now turned a single dollar into $1 million. Buffett joked that surely some players would also experience an exponential rise in confidence, impelling those players to “write books on ‘How I Turned a Dollar into a Million in Twenty Days Working Thirty Seconds a Morning.'”

We can see that kind of irrational exuberance proliferating today, with constant market highs, meme stocks and the launch of various cryptocurrencies. It’s easy to feel like a genius when everything is going up, just as it’s easy to feel like a genius flipping a coin. It doesn’t mean any of it is good for you over the long term.

As an investor, it’s important to know your sources. The investments you choose are like the foods you eat. You don’t need all that complex, artificial stuff with lab-engineered ingredients you can’t even pronounce, either in your diet or your portfolio, when simple will do.

If you don’t know what you’re picking is ripe, then it’s you who is ripe for the picking.

How do you choose?

Take it from Bogle, who wrote in The Little Book of Common Sense Investing:

“When there are multiple solutions to a problem, choose the simplest one.”

8 thoughts on “You Are What You Eat — and Invest”