In the discussion of the single most important financial asset — investments, pension, real estate, cash, etc. — I nominate the body. Your body is how you make a living. And in a flash or rising crest, your body can come to dictate your entire financial life.

This is evidenced by the more than 80% of older adults who say maintaining health and wellness is the most important goal throughout retirement, while a common retirement dream like traveling became significantly less important (Employee Benefit Research Institute’s Spending in Retirement Survey).

Who wants to think about that though?

I’m a couple years shy of 40 and fortunate to have good health with a relatively clean family medical history. I should be concentrating on hitting my peak earning years and living life to the fullest. So, why do I want to think about aging and the inevitable decline of one’s health?

Because sometimes the world has a way of reorienting your focus. Observation is an underrated practice for growth — in work, relationships and money. Look at the things and people around you and ask: Is this related to my situation today? Could that be me some day?

Life is a game with many rules but no referee. One learns how to play it more by watching it than by consulting any book.

JOSEPH BRODSKY

That’s what happened to me.

I live in a sleepy neighborhood where many older adults choose to retire in place. Surrounded by neighbors in their 60’s, 70’s and 80’s, the visages of old age are highly visible. One day someone starts walking with a cane. Sometimes someone disappears for days and suddenly a “for sale” sign appears in their front yard. And the alternating red-and-white glow of ambulance lights streaking by at night is not a rare occurrence.

My next door neighbor, Rick, is a retired firefighter. His wife suffered a stroke several years ago and rarely ventures outdoors. They have no children and no close relatives that I know of. This past week, I happened to be outside while Rick mowed his front lawn. Half way through, he cut the engine and shuffled to his front porch to sit down. I could tell something was wrong, so I walked over to check on him. He was slumped over with hands on his knees, breathing heavily. He tied to brush it off. But finally, with much objection, he agreed to let me help finish cutting the grass then and throughout the summer.

It was a simple neighborly gesture, yet with a terrible weight of significance. Someone who once charged through burning buildings was now essentially beaten by the tension of a push lawn mower. This was the day when a mundane house chore had exceeded his physical abilities. A day that is likely in all our futures. He now had to accept what we never want to accept, or even think about.

So, I wonder what Rick, with an ill spouse and no children, will do if he needs long-term care?

If you don’t know or never cared to know, long-term care is the range of health care services for someone suffering from a chronic illness or disability over an extended period of time. It is a growing challenge in America. As we live longer, growth in the number of older adults is unprecedented. In 2016, Census data shows 15% (49.2 million) of the U.S. population was aged 65 or older and is projected to reach 23% (95 million) by 2060.

This being America, there is no simple, obvious solution. On top the potential indignity of diminishing physical and mental capacities, in America, you are given the task of navigating a complex labyrinth of funding options to pay for the care you need without having to place the burden on the shoulders of a loved one.

And so, after the experience with my neighbor, I can’t help but also wonder: How early is too early to think about long-term care?

The impact of long-term care

If you want to understand what this all may mean for you, there is no better resource than Christine Benz’s insightful Morningstar article “100 Must-Know Statistics About Long-Term Care.”

Here are some of the eye-opening highlights:

Who needs it

- 70% of people turning age 65 who will need some type of long-term-care services in their lifetimes.

- 48% of people turning age 65 who will need some type of paid long-term-care services in their lifetimes.

- 3.7 years is the average duration of long-term-care need for women.

- 2.2 years is the average duration of long-term-care need for men.

Cost of care

- 63% of individuals age 65 today will have no out-of-pocket long-term-care costs during their lifetimes… but if you do:

- $321,780 is the estimated lifetime cost of care for someone with dementia.

- $51,600 is the median annual cost for assisted-living facility (2020).

- $54,912 is the median annual cost for a home health aide (44 hours/week; 52 weeks/year, 2020).

- $105,850 is the median annual nursing-home cost for a private room (2020).

- $142,254 is the expected median annual nursing-home cost for a private room in 2030 (assuming 3% inflation rate).

- $256,926 is the expected median annual nursing-home cost for a private room in 2050 (assuming 3% inflation rate).

How long-term care can impact your wealth

- 20% is the median increase in household wealth over a nine-year period for married people ages 70 and over who did not require long-term care.

- -21% is the median decrease in household wealth over a nine-year period for married people ages 70 who had a long-term-care need.

Who provides care

- 41 million people provide unpaid care for family members in the U.S. (2015).

- $470 billion is the estimated dollar value of long-term care provided by unpaid caregivers (2013).

- 69.4 is the average age of care recipients.

- 62.3 is the average age of spousal caregivers.

- 34% of caregivers are age 65 or older.

As with many American household challenges, a greater burden is placed on the shoulders of women:

- More than 75% of caregivers are female.

The potentially steep cost and heavy burden of long-term care emphasizes the importance of early planning. Especially, for those with family histories of severe cognitive impairment, a condition that requires high levels of service for long periods of time.

Long-term care funding options

The difficulty is determining how to cover long-term care when you’re only working with probabilities of how much care you need, if you ever need it.

Depending on the severity, there are not a lot of great options.

People generally choose from a handful of ways to pay for long-term care expenses. One of which is not Medicare — at least not as a reliable long-term option. Medicare primarily pays for “medical services,” whereas long-term care primarily consists of “custodial services.”

(Note: This is a simple overview. The various strategies within each option are far too complex to cover in detail here.)

Self-funding

“Self-funding” involves using income, retirement savings, investments or other assets, such as home equity, to pay for care. You can either draw from the wealth you’ve amassed or build a reserve specifically for long-term care expenses.

This option allows people to avoid having to pay insurance premiums or arrange care through a government program. Mainly, those who have substantial income or wealth and clean family medical histories are best suited to pay out of pocket.

Long-term care insurance

Insurance is one way to hedge against the high cost of care. When long-term care is needed, a person’s assets are better protected when more of the costs are covered through the benefits provided by insurance.

Basically, long-term care insurance pays a daily amount, up to a predetermined limit and length of time, for qualified services. Those factors, along with any optional benefits, generally determine the cost of premiums.

Age is another major factor. The average long-term care insurance buyer is around 57. The older a person is, the more expensive the policy will be. Insurers can also reject or place care limitations on those who are in poor health or have pre-existing conditions.

Insurance can provide piece of mind, but could become a financial strain as rates rise with age and should you never use it. The average annual long-term-care premium for a 55-year-old male (initial pool of benefits worth $164,000) is $1,870. For a 55-year-old female, the average annual long-term-care premium (initial pool of benefits worth $164,000) is $2,965.

Buyers must pay for premiums consistently for many years or let it lapse, meaning that money was wasted. That sums up the experience of a third of people with long-term care insurance who at age 65 let their policies lapse.

Those with moderate financial means may consider insurance as a way to reduce the risk that long-term care expenses will deplete their financial assets.

Hybrid life insurance with long-term care benefits

Under a life insurance policy with long-term care benefits, policyholders are guaranteed to be paid one benefit. Premiums paid go toward a policy that can be used for long-term care.

The policy then pays a tax-free death benefit to beneficiaries, depending on how much of the long-term care benefit is used. That means the more of the benefit that is used for long-term care, the less that is available for beneficiaries. As with long-term care insurance, the features of these combination products can vary widely.

People in good health and with good family medical histories who want the assurance insurance can provide yet hope to leave an inheritance may find incorporating life insurance into their long-term care strategy an attractive option.

Medicaid

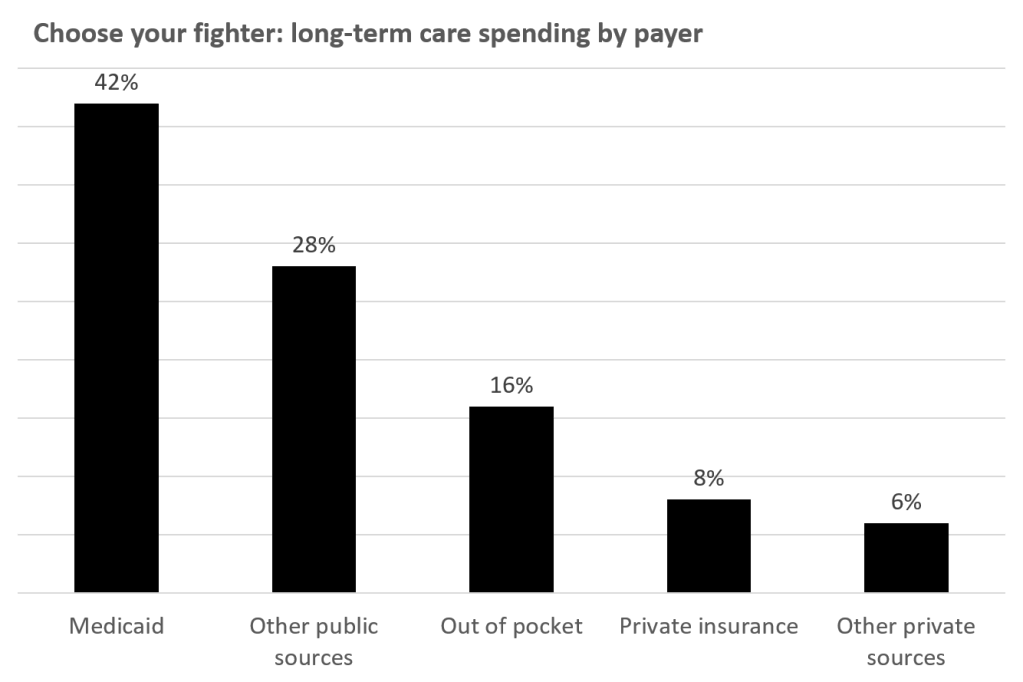

Medicaid, the government program designed to provide medical care for those with limited resources, is the primary payer for formal long-term care, covering about 42% of all long-term care spending.

Unlike Medicare, Medicaid does provide for custodial care, including long-term care services in nursing homes and services provided at home, such as visiting nurses and assistance with personal care. Medicaid programs and the services provided vary state by state.

But here’s the thing: you may have to use up most of your assets paying for your long-term care before Medicaid is able to help. Many people start paying for care out of pocket and “spend down” their income and assets until they are eligible for Medicaid.

Generally, Medicaid is for those who have limited savings and cannot afford long-term care insurance or were denied coverage. Typically, to qualify for Medicaid, an individual is only allowed to have $2,000 in countable assets. Hence, Medicaid is commonly considered the option of last resort.

The best option varies from person to person, depending on personal factors including: income and assets, current health, family medical history, and whether family or friends can provide support.

Everyone though should have a discussion with loved ones about how they want to be cared for if long-term care is necessary. And, considering the complexity and costs of long-term care, it’s beneficial to work with a professional, such as a financial adviser or elder law attorney, who can help determine what option is most appropriate for your situation.

One way to improve your chances of making the right decision is to plan as early as possible. That starts with your most important financial asset.

One long-term care solution for today

So, how early is too early to think about long-term care? It’s never too early.

Because it’s never too early to think about making choices to live a long, meaningful, healthy life. Today’s decisions become tomorrow’s realities.

Therefore, one important financial step to take now is to protect that number one asset: your body. Without it, nothing else really matters.

As with most financial advice — live within your means, pay yourself first, etc. — there is no secret to living a healthier life: eat a balanced diet and regularly exercise. Those two things alone have been linked to lower risks of many physical and mental ailments.

But don’t forget about sleep. A recent report found that middle-age adults who sleep six hours or less a night may be more likely to develop dementia in their late 70’s.

There is a strong relationship between health and wealth, as detailed in a paper from Rutgers University.

Some of its findings:

- The Centers for Disease Control estimates that a 10% weight loss could reduce an overweight person’s lifetime medical costs by $2,200 to $5,300.

- Inactivity has been estimated to cost between $670 to $1,125 per person per year.

- Healthy people (non-smokers and those in normal weight ranges) pay lower premiums (preferred rates) for life insurance, compared to smokers and those who are overweight.

- One-quarter (26%) of respondents to the 2005 Health Confidence Survey, sponsored by the Employee Benefit Research Institute, reported that they decreased their contributions to a retirement savings plan as a result of the increased cost of health care and 45% reported decreasing other savings.

- According to a study by The Rand Corporation, obese individuals also spend about 36% more than average-sized people on health services and 77% more on medications.

Further, a 2019 study published in the American Journal of Public Health estimates around 66% of Americans declared bankruptcy because of medical issues. For example, being unable to pay their medical bills or losing time from work.

The financial benefits of improved health behaviors are unquestionable. Lower health care costs mean more income available to save and invest for your financial goals. A healthier, longer life means more time to work and take advantage of the power of compound interest.

Of course, none of these unsentimental numbers may convince anyone to change their lifestyle. We all know the benefits of a healthy lifestyle. It is so easy, yet we often fail. (As I type this with a pint of beer, I know I do!)

What will change is that one day it will become personal, either to you or someone you know. As the simplest tasks become too great, we are assigned the hardest task of all — to ask for help.